Redesigning the Mobile

Banking Experience for

India's No.1 Bank

The Team & My Role

Led end-to-end design for the project, managing a multidisciplinary team and collaborating closely with cross-functional stakeholders across the organization

Internal

- Role

- Lead Designer

- Design Team

- 5 Product Designers

- Motion & Illustration

- On-demand specialists

- Project Manager

- Delivery & Coordination

Client

- Product Team

- Requirements & Prioritisation

- Engineering Team

- Feasibility & Implementation

- Experience Design Team

- Alignment & Collaboration

- C-Suite

- Workshops & Strategic Direction

The Challenge

Bridging the gap between digital capability and modern user expectations for 12 crore users

HDFC Bank has long been a digitally progressive institution, but its mobile experience had not kept pace with evolving user expectations and advancements in the ecosystem. Key journeys presented opportunities to reduce friction, improve accessibility, and create a more cohesive, modern experience.

-

Fragmented user base. We need to bring bank branch users and net-banking users to the mobile app. Only 50% of HDFC Bank users use the mobile app"

— Chief Digital Officer -

There's too much friction when it comes to making transactions. Core payment functionality like recurring payments and UPI are missing"

— Product Team representative -

Users are highly dependent on the Customer Support Team, overwhelming the support function. We need the app to be self sufficient, and more user friendly"

— Customer Support Team representative

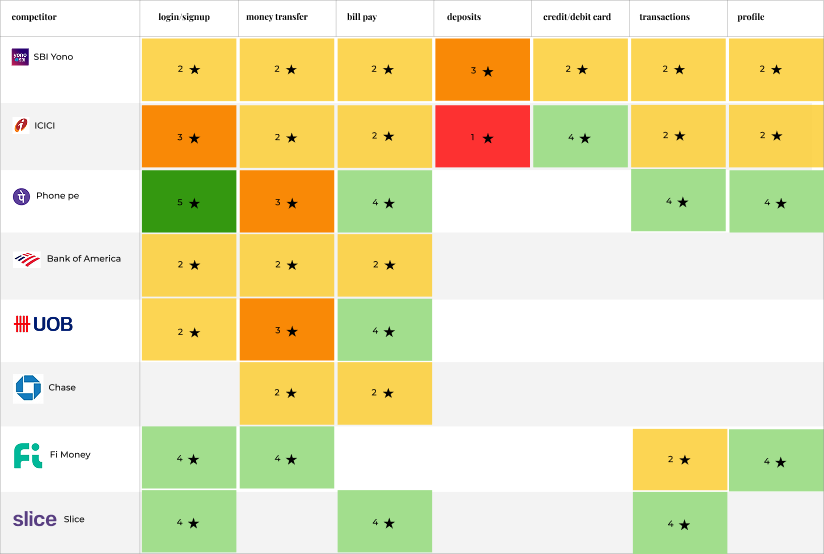

Research & Discovery

Direct user access was limited, so we triangulated insights through stakeholder interviews, workshopping, and competitive benchmarking.

- Stakeholder interviews across customer support, product, engineering, and branch operations

- Workshops with leadership to align on vision and principles

- Strategic benchmarking (best-in-class products like Airbnb, Uber)

- Tactical benchmarking (banks, fintech apps, neo-banks)

Insights

Key product and experience gaps impacting adoption

-

Transaction Friction

High-frequency actions like payments were not optimised for speed or accessibility, increasing reliance on alternative apps for everyday banking.

-

Support Dependency

Users depended on customer support for basic tasks, indicating gaps in product clarity, self-service design, and in-app guidance.

-

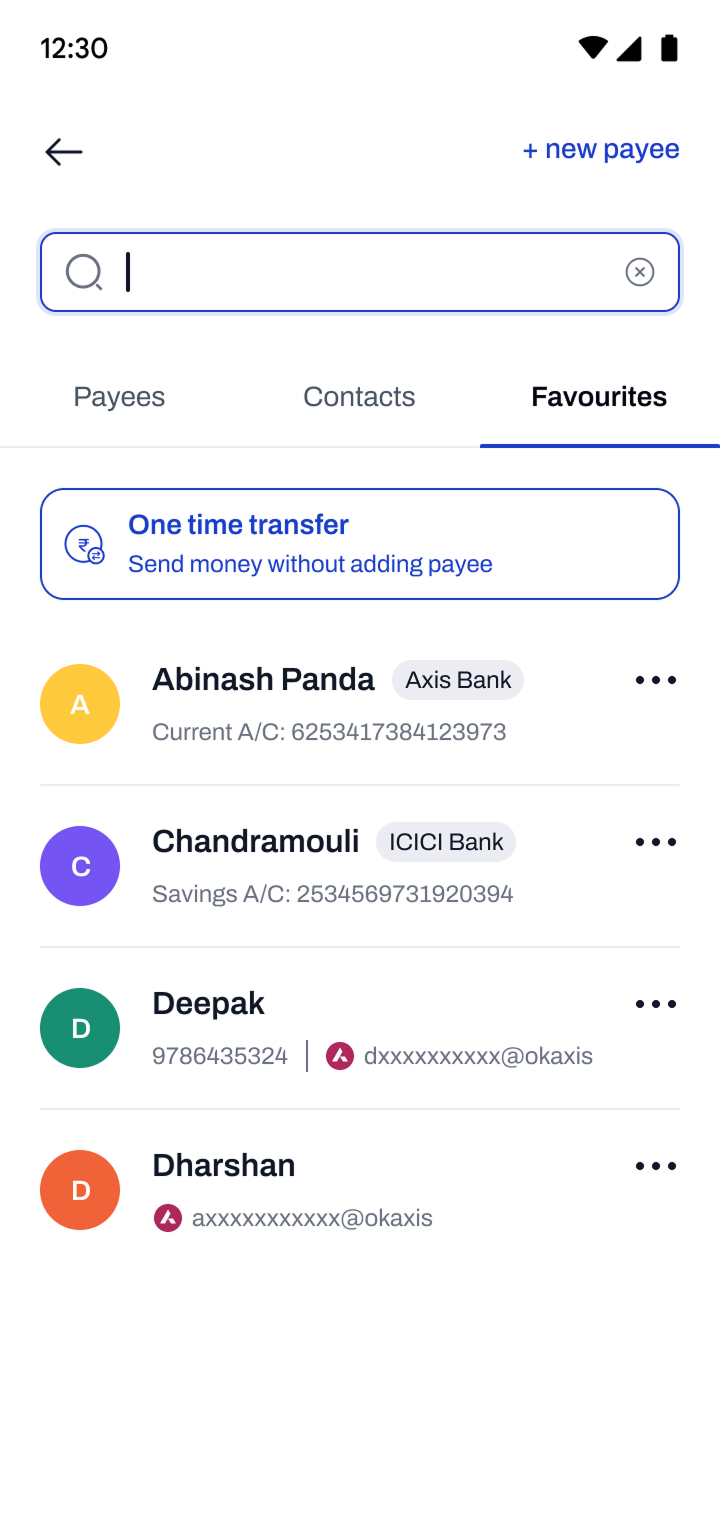

Fragmented User Base

User segments were fragmented across channels — branch, NetBanking, mobile — limiting adoption of the app as a primary banking interface.

-

Onboarding & Access Friction

Onboarding and access flows introduced uncertainty and friction, causing drop-offs before users experienced any product value.

Constraints & Guardrails

Balancing usability with compliance, trust, and system realities

-

Regulatory Compliance

Key flows like onboarding, authentication, and data access had to meet strict regulatory requirements, limiting how much friction could be removed.

-

Security & Trust Sensitivity

Users were cautious about sharing personal and financial information, requiring clearer communication rather than reducing safeguards.

-

Existing Mental Models

Users relied on familiar banking patterns, making it important to align new interactions with established expectations.

-

System-Driven Dependencies

Backend processes such as customer data fetching and device binding constrained how certain flows could be simplified.

-

Diverse User Base

The experience needed to work across varying levels of digital literacy, requiring clarity, guidance, and reduced cognitive load.

Process Artefacts

Supporting research and exploration

-

Competitive Benchmarking

-

Discovery Workshops

-

Information Architecture

Users

Designing for a diverse and fragmented user base

Through stakeholder interviews and internal research, we identified distinct user behaviors and needs across HDFC's customer base. These patterns helped us simplify complexity into clear user segments that directly informed key product decisions.

-

Digitally Active

Comfortable with fast payments and expect minimal friction

Enabled fast-access features like pre-login UPI and reduced interaction steps.

-

Low-Confidence / Assisted

Depend on support and need clarity in flows

Shaped guided onboarding, contextual help, and transparent permission flows.

-

Existing but Inactive

Already bank customers but not mobile users

Influenced multiple registration methods and inclusive access.

Strategy

Defining product bets and design principles to guide the experience

The research revealed systemic gaps across onboarding, access, and core journeys. We translated these into a set of product-level bets and guiding principles to improve activation, engagement, and long-term adoption.

Product Bets

-

Reduce friction at entry

Improve onboarding completion and activation

-

Enable self-sufficient usage

Reduce dependency on support

-

Unlock existing user base

Increase activation without new acquisition

-

Increase frequency of use

Drive engagement through faster access

-

Establish a scalable design foundation

Improve consistency and long-term usability

Design Principles

-

Deep Empathy

Design with a clear understanding of user context, constraints, and behavior — especially in high-stakes financial interactions.

-

Progressive Inclusivity

Create experiences that work across varying levels of digital familiarity, access, and confidence.

-

Positive Surprise

Introduce moments of delight within functional flows to make the experience feel engaging and human.

-

Evolve & Adapt

Continuously evolve patterns and interactions to meet changing user expectations and technological advancements.

-

Simplicity

Prioritize clarity and ease of use, reducing complexity in critical journeys to enable faster, more confident actions.

These principles and bets guided decision-making across the entire product.

Product Decisions

Shaping core journeys through key product decisions

-

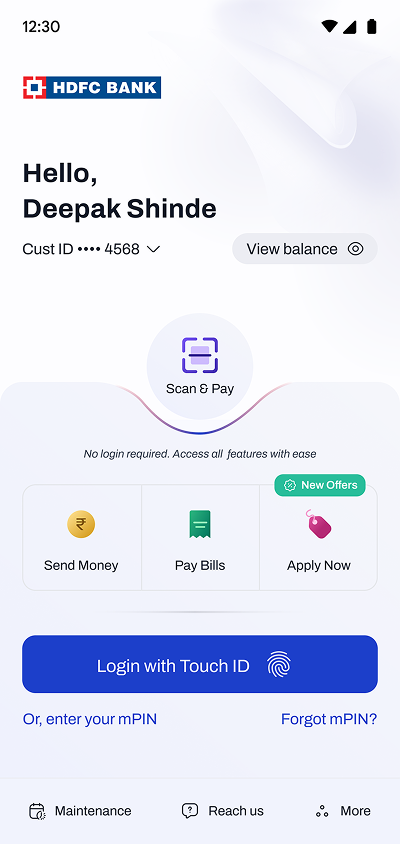

Decision 01

Transactions without login

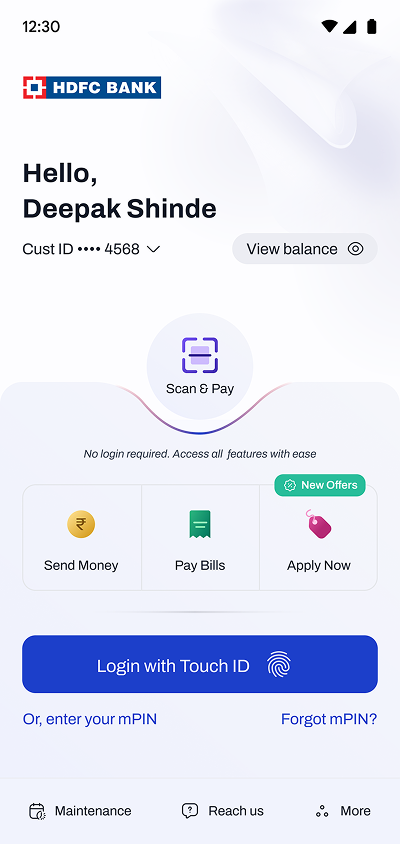

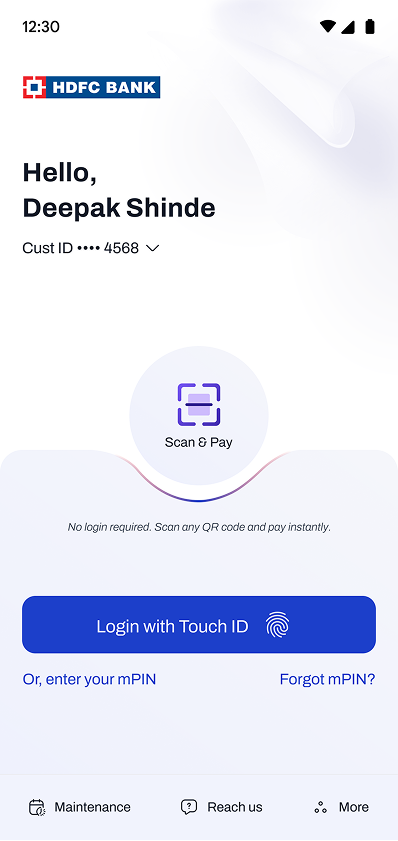

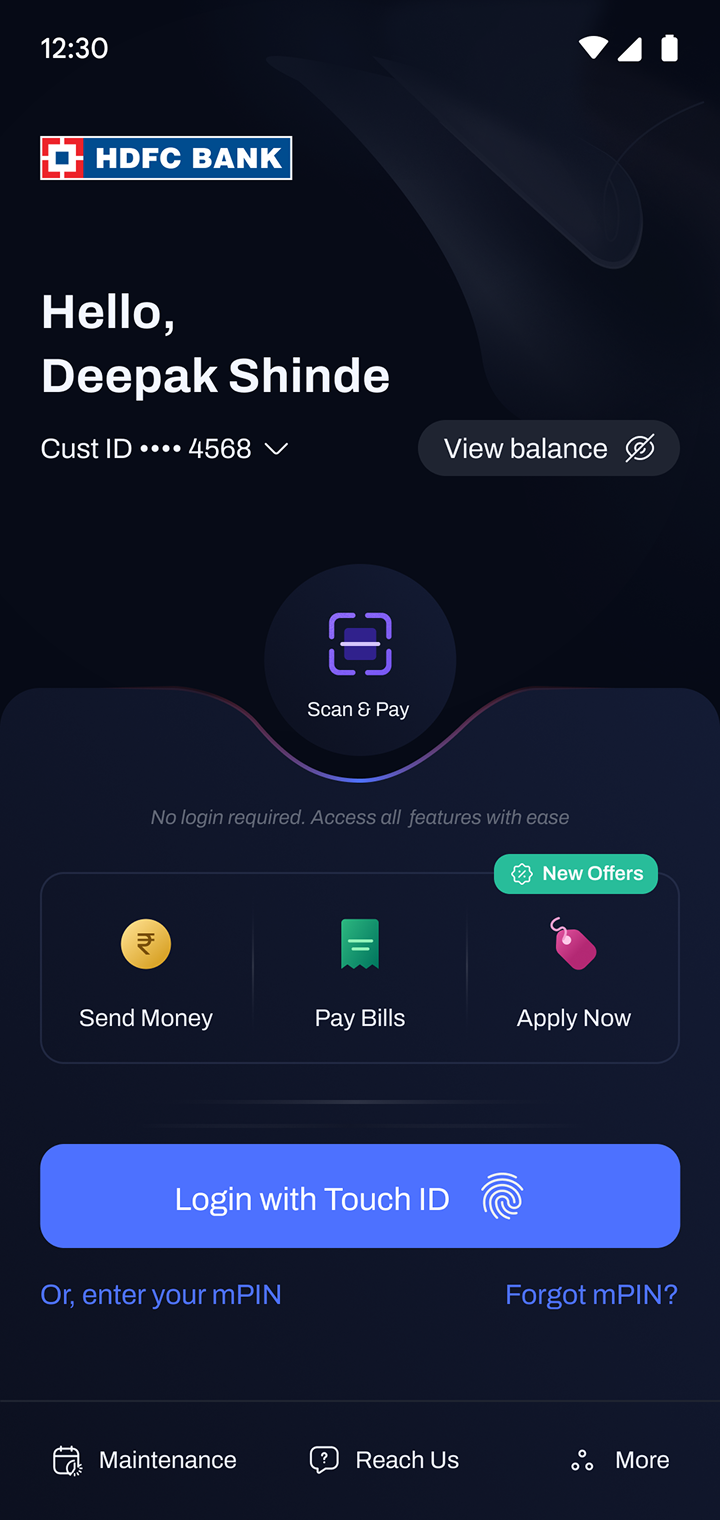

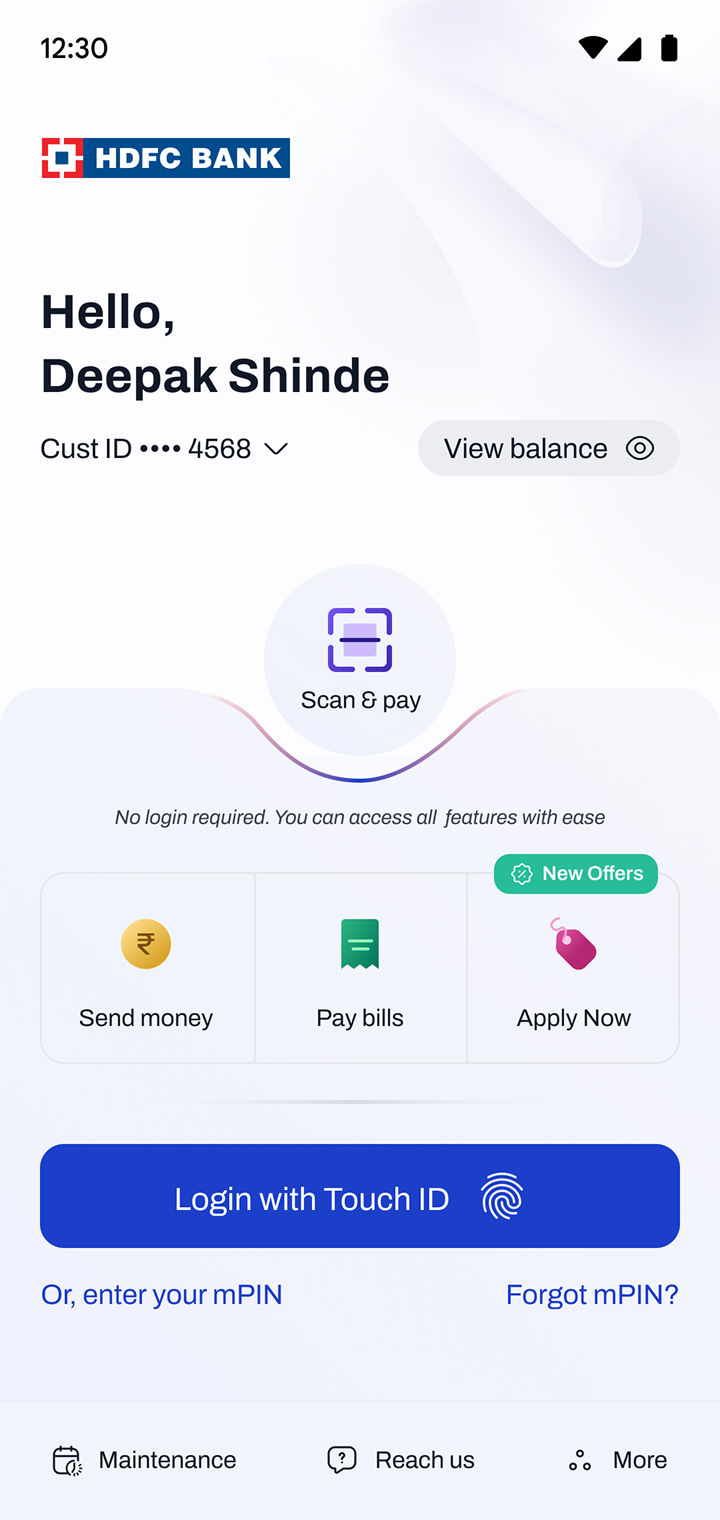

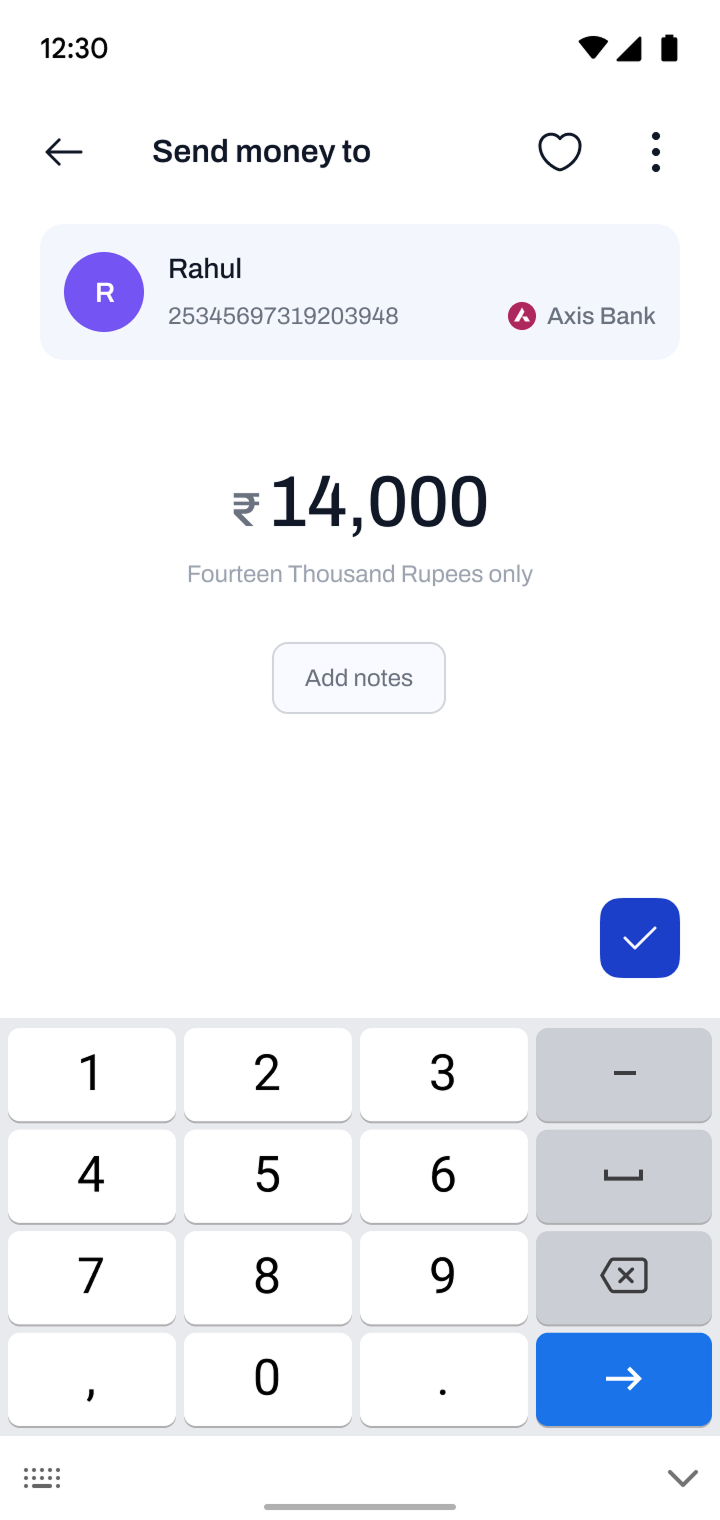

We had to make a tradeoff between security perception and transaction speed. Existing solutions — biometric shortcuts and wallet-based access — still required an authentication step at the point of use. We moved to full transactions without login, making HDFC Bank the first bank in India to offer this. The decision directly addressed users' growing expectation for fast, frictionless payment access — shaped by increasingly seamless experiences across the payments ecosystem.

Business Intent

- Transactions per User (TPU)

- DAU / MAU Stickiness Ratio

- Time to First Transaction (TTFT)

Tradeoff

Convenience vs Security Perception

Maintaining auth was costing adoption without proportionally protecting trust.

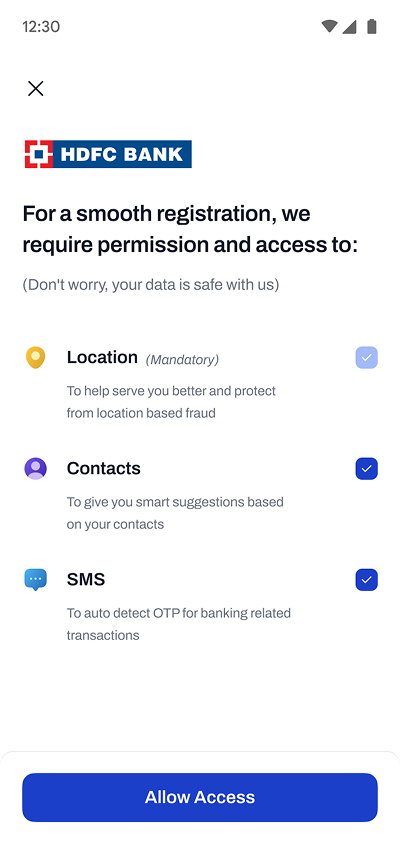

-

Decision 02

Thoughtful permissions

Permissions were system-driven interruptions with no context, causing hesitation in a high-trust environment like banking. Users felt a loss of control. We reframed permissions as transparent, user-driven decisions — balancing critical requirements with trust and choice.

Business Intent

- Permission Acceptance Rate

- Permission Step Drop-off Rate

- Feature Activation Rate (UPI, Contacts)

Tradeoff

Feature Activation vs Trust

Banking onboarding is the wrong moment for aggressive permission requests.

-

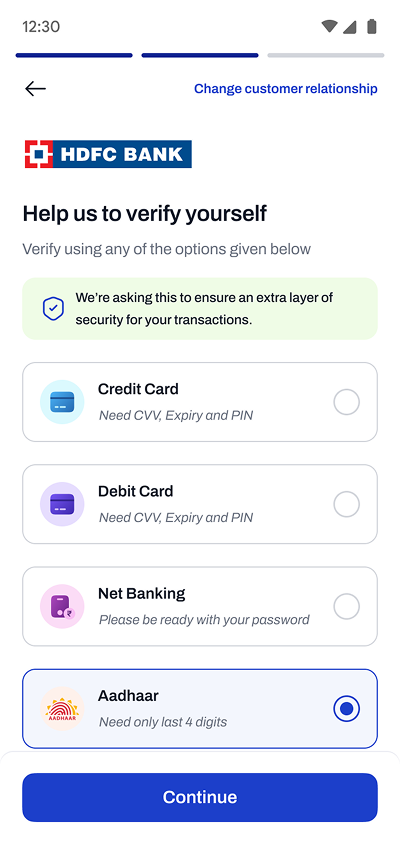

Decision 03

Multiple verification methods

Registration relied on fixed credential-based flows. When required information wasn't available, users dropped off and abandoned entirely. We introduced a flexible approach letting users choose their easiest path and recover from errors without exiting the flow.

Business Intent

- Registration Completion Rate

- Mid-Funnel Drop-off Rate

- Account Activation Rate

Tradeoff

System Complexity vs User Simplicity

Complexity absorbed by the system, not passed to the user.

-

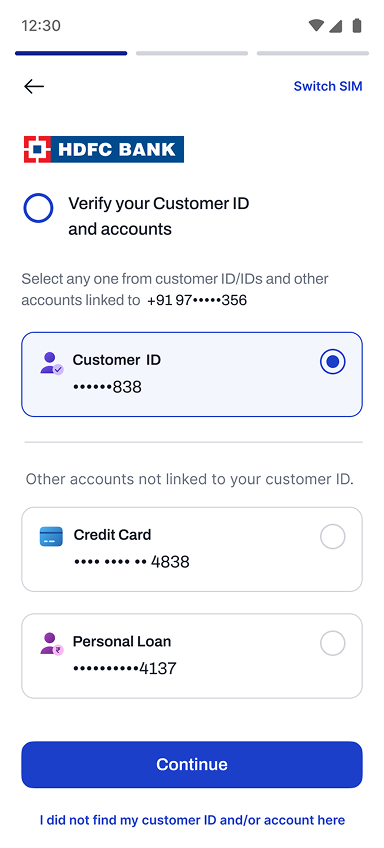

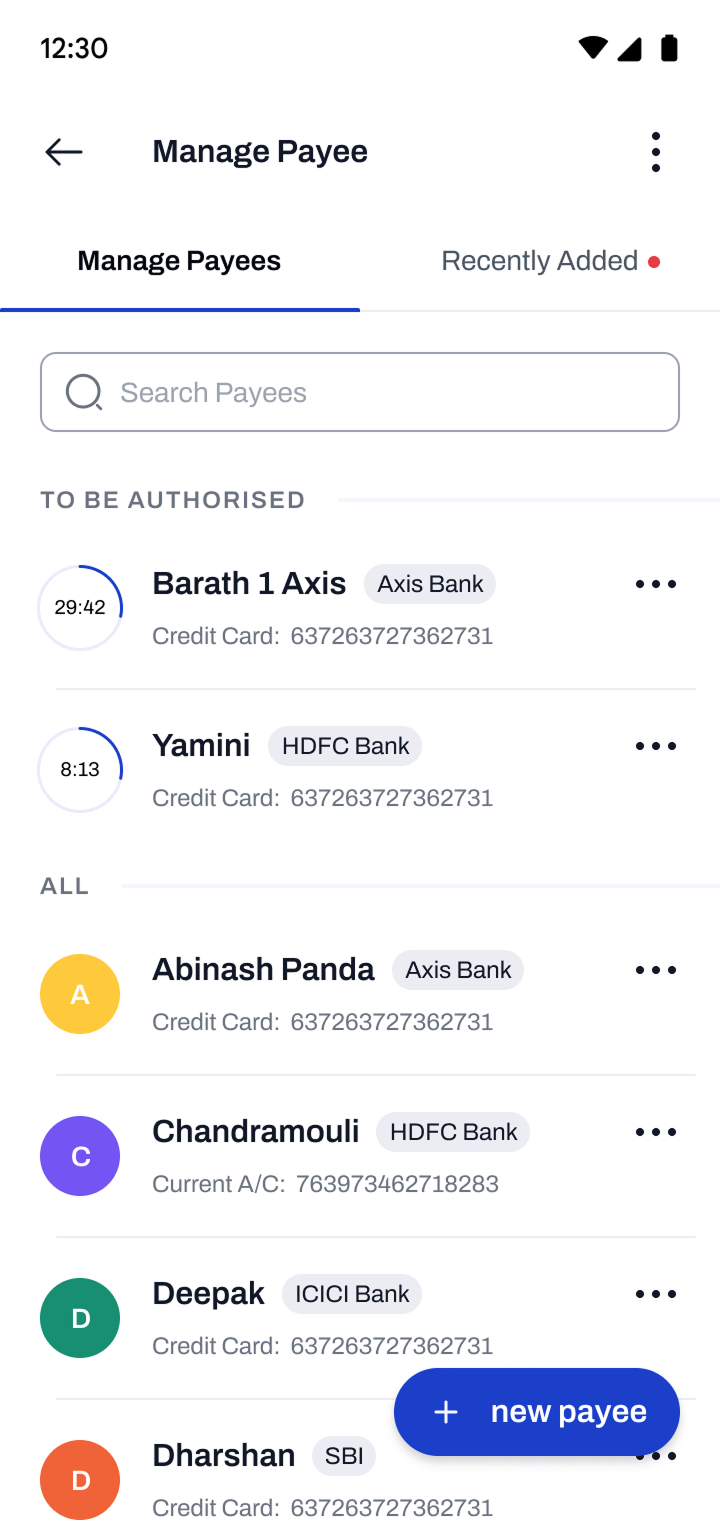

Decision 04

Inclusion of legacy users

A large portion of existing customers used NetBanking, credit cards, or branch services — with no seamless path into the app. We unified entry points so existing users could transition without additional friction.

Business Intent

- Activation Rate (Existing Customers)

- Customer Acquisition Cost (CAC)

- Products per User (Cross-sell Rate)

-

Decision 05

Adapting to different user needs

A single interface couldn't serve both confident and low-confidence users effectively. We introduced Simple and Power versions of the pre-login experience — letting users choose during registration with the flexibility to switch later. Same product, two levels of complexity.

Business Intent

- Feature Engagement Rate (Segment-wise)

- Sessions per User

- User Retention D/D

Pre-Login / Power

Pre-login / Simple

-

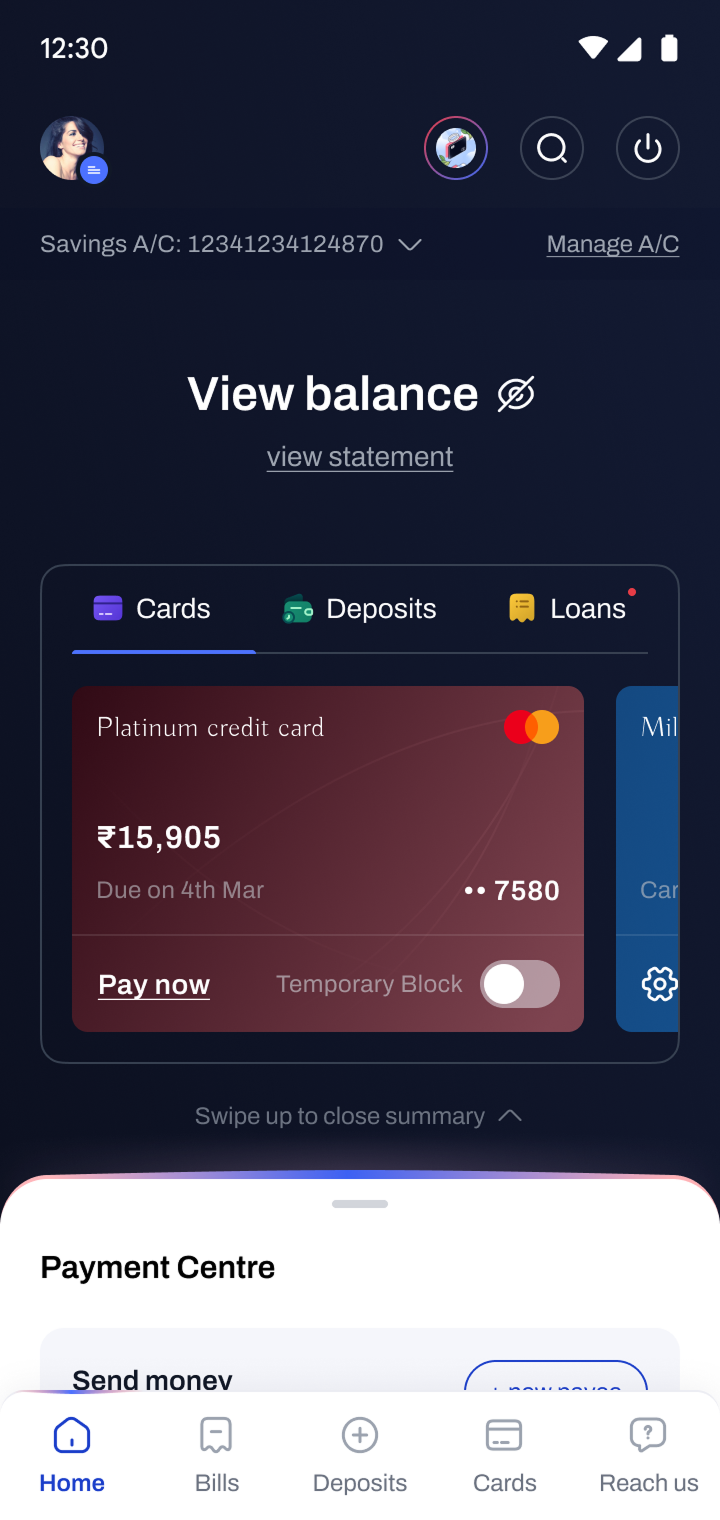

Decision 01

Key revenue drivers given highest priority

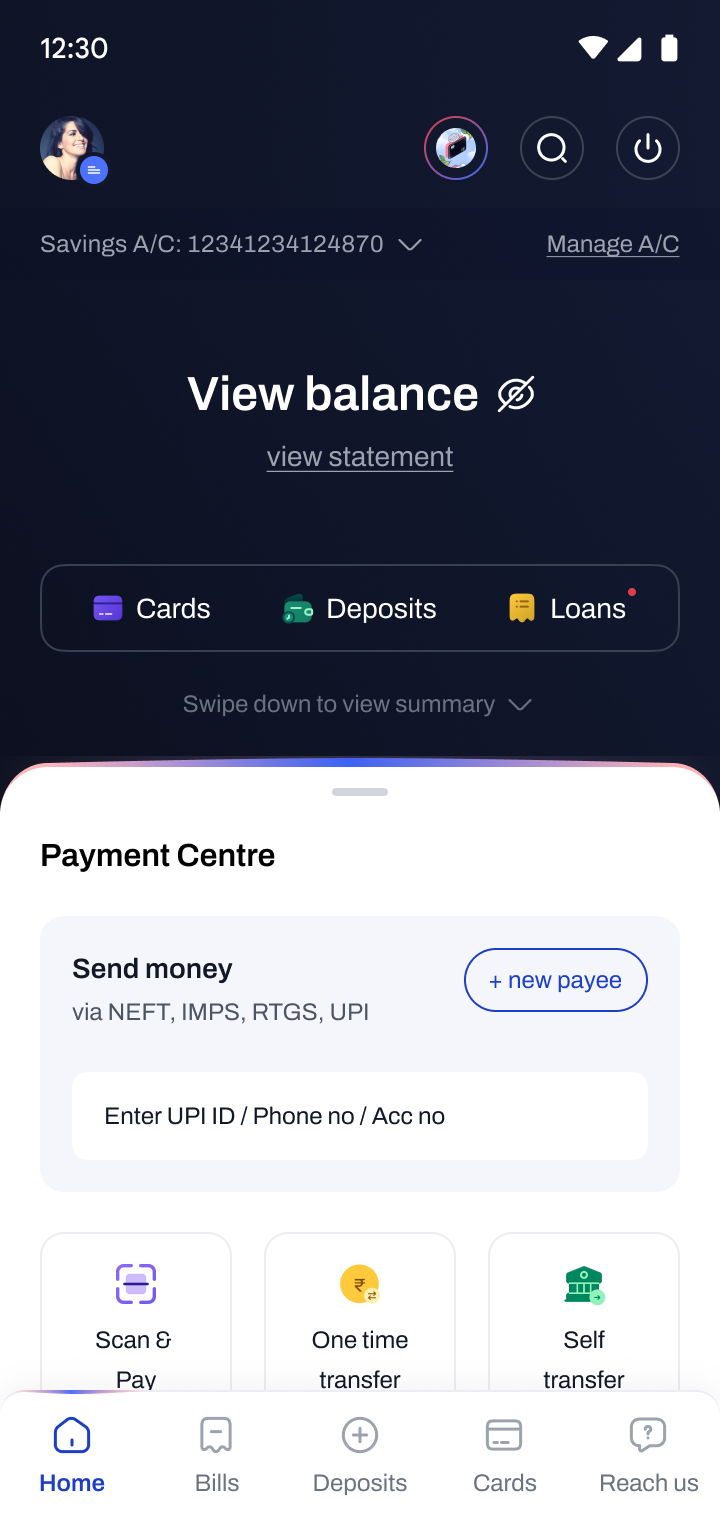

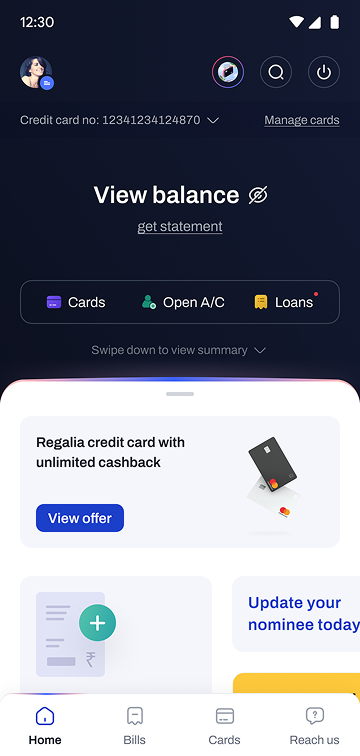

Cards, Deposits, and Loans are HDFC Bank's key revenue drivers. We gave them prime screen real estate with custom icons to draw attention. Deposits and cards are also accessible from the bottom navigation — never more than one tap away.

Business Intent

- Product Adoption Rate (Cards, Loans, Deposits)

- Conversion Rate

- Revenue per User (ARPU)

-

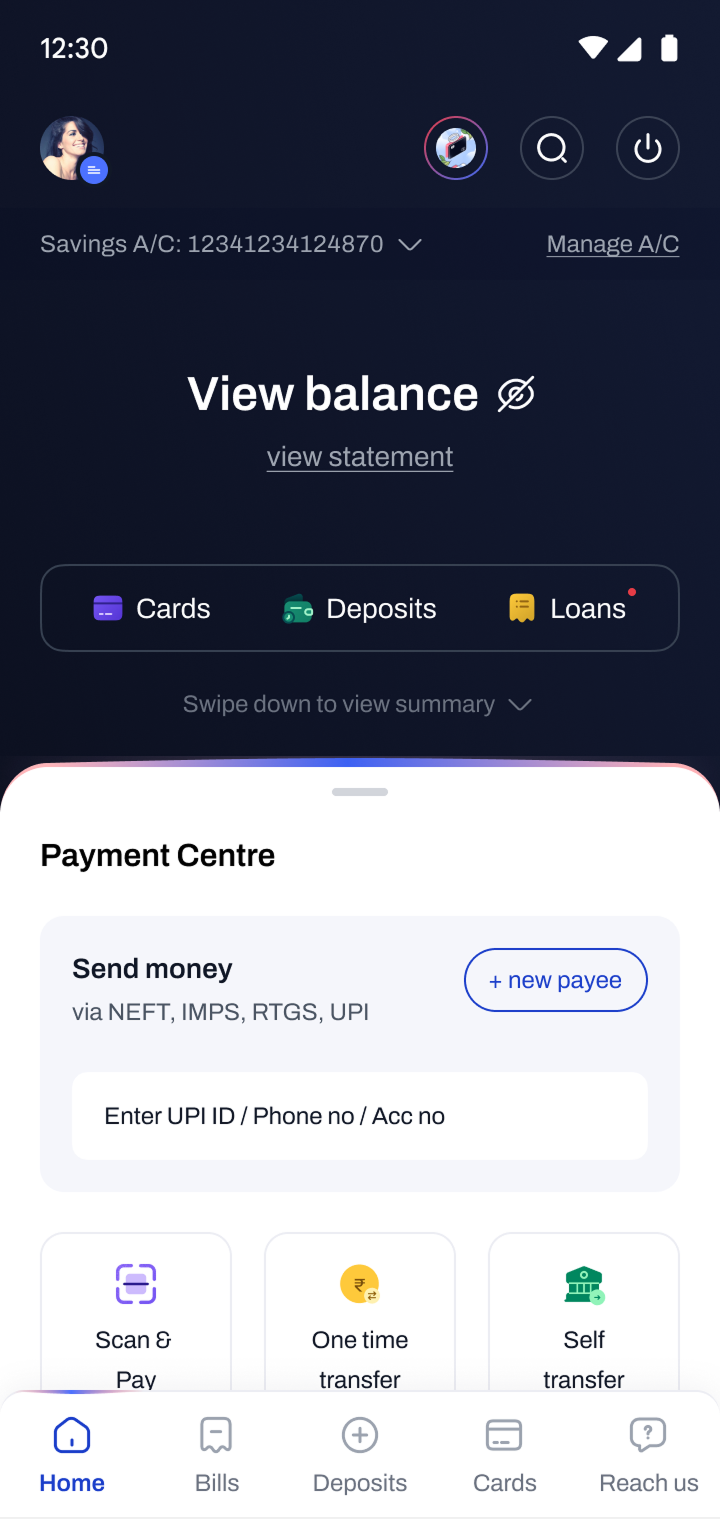

Decision 02

Unified payment component

Payments were scattered across multiple entry points, creating friction and confusion. We consolidated all payment actions into a single, consistent component — reducing cognitive load and improving discoverability of core transaction flows.

Business Intent

- Transaction Completion Rate

- Time to Complete Transaction

- Transactions per User (TPU)

-

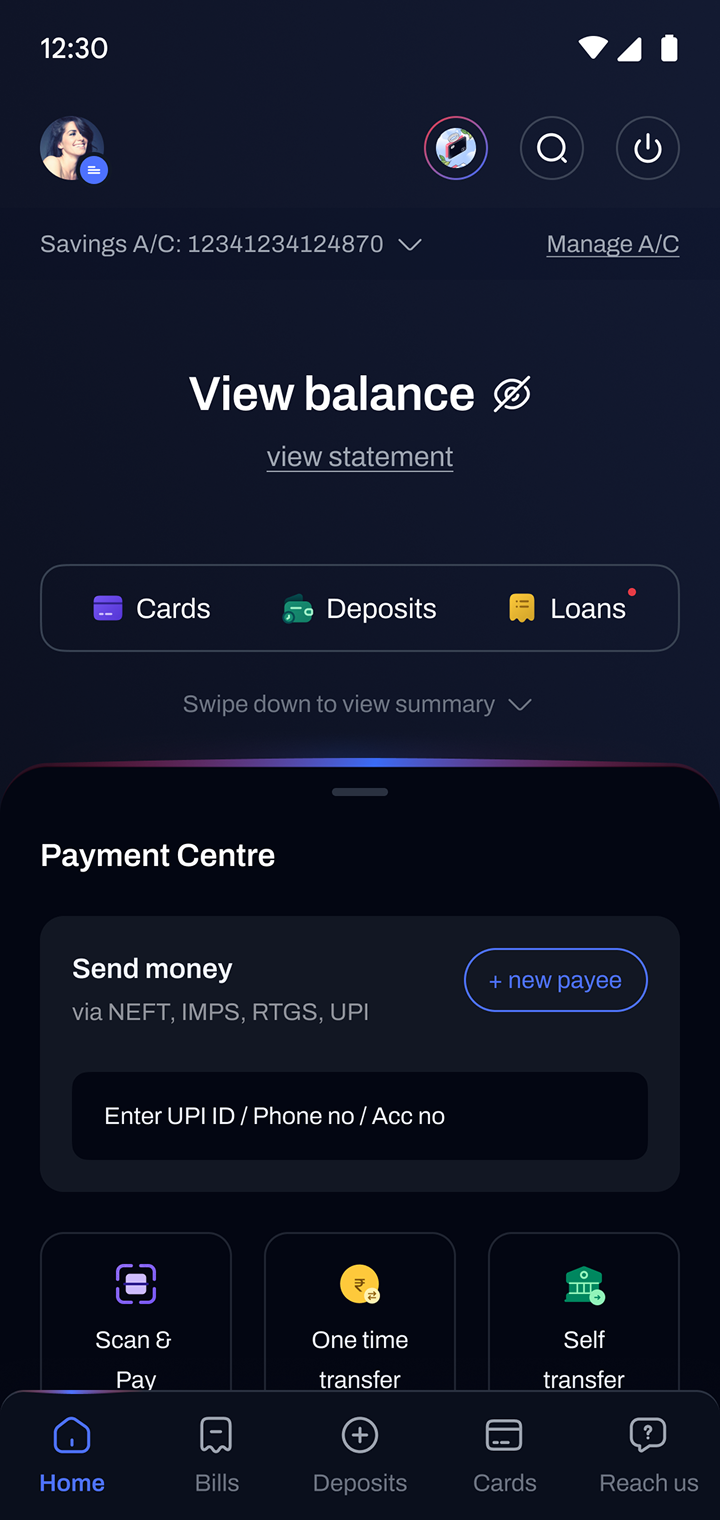

Decision 03

Account balance hidden by default

A common concern was strangers glimpsing the balance when the app was open in public. Hiding it by default was a simple but powerful change — addressing a real user anxiety and enabling more confident, everyday usage.

Business Intent

- User Trust (Perceived Security)

- App Open Rate

- User Retention D/D

Tradeoff

Visibility vs Privacy

One extra tap costs less than the anxiety of exposed finances in public.

-

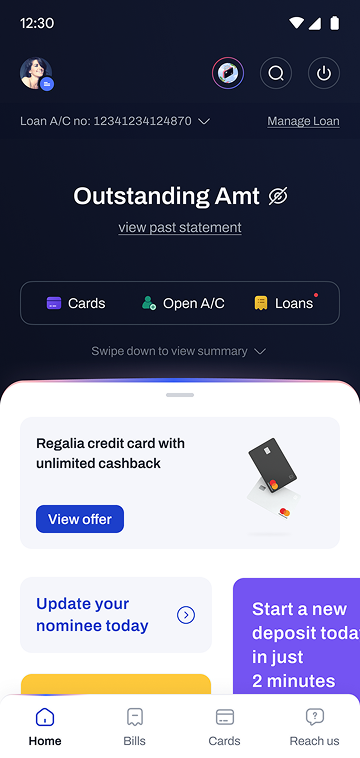

Decision 04

Inobtrusive ads and nudged offers

Users consistently complained about intrusive ads. We addressed this with a dedicated offers section styled like Instagram stories, accessible on demand, and strategic cross-sell nudges based on user preferences — replacing disruption with relevance.

Business Intent

- Offer Engagement Rate

- Offer Conversion Rate

- Ad Dismissal / Ignore Rate

Tradeoff

Commercial Goals vs User Experience

Trust across many sessions is worth more than conversion in a single one.

-

Decision 05

Personalized dashboards per user segment

One dashboard couldn't serve all users effectively. We designed multiple versions — Standard, Standalone Credit Card, Standalone Loan, and Secondary Account — tailoring content and hierarchy to each profile without increasing overall complexity.

Business Intent

- Feature Engagement Rate (Segment-wise)

- Session Depth (Features per Session)

- User Retention (Segment-wise)

Standalone Loan

Standalone CC

-

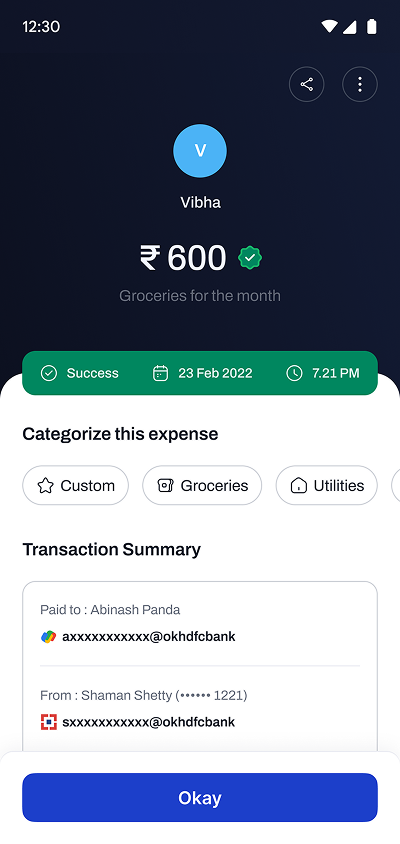

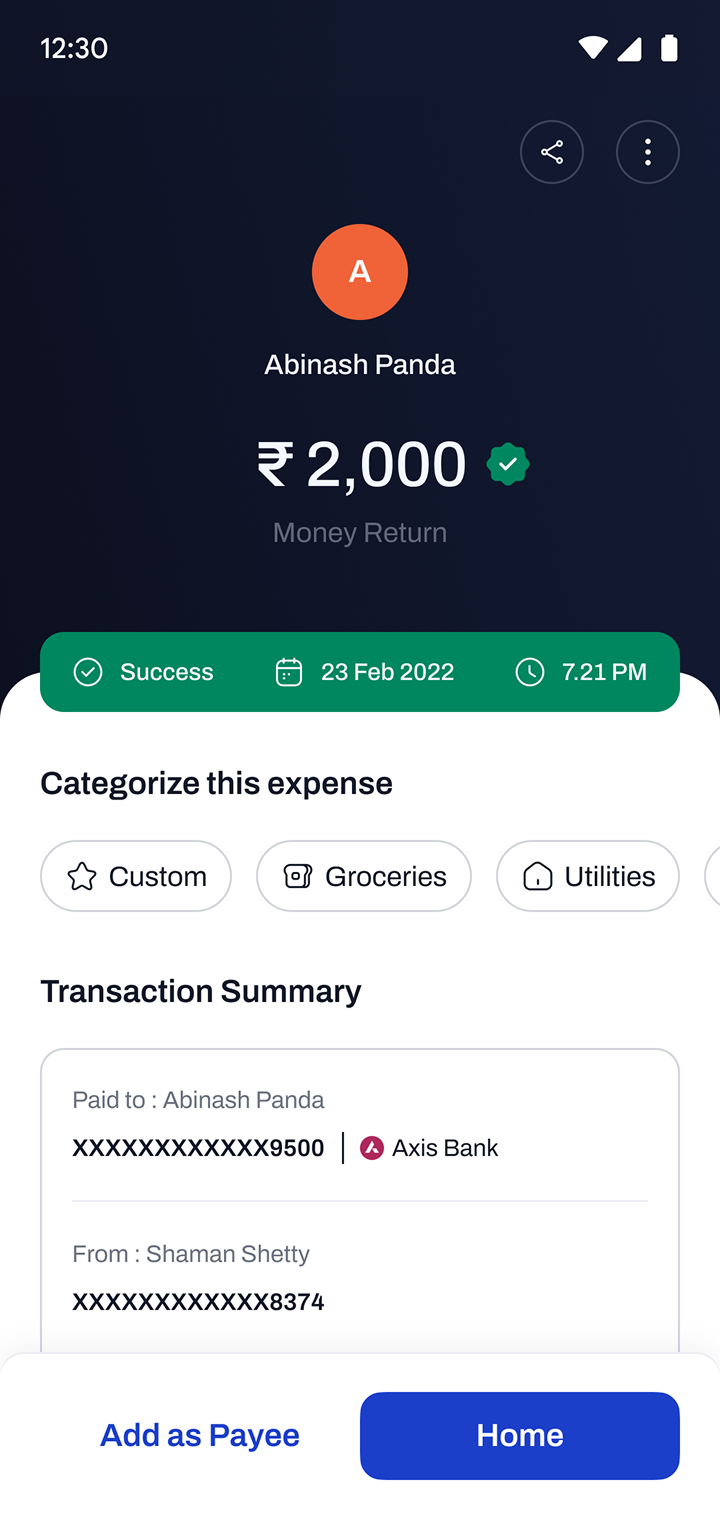

Decision 01

Overhauled transaction summary

The existing summary lacked hierarchy and was cluttered, making it hard to understand status or take follow-up action. We improved hierarchy, used colour to distinguish success, failure, and pending states, introduced transaction categories, and made sharing send a screenshot automatically.

Business Intent

- Transaction Review Engagement (Views / Time Spent)

- Follow-up Actions

- Transaction Support Queries

-

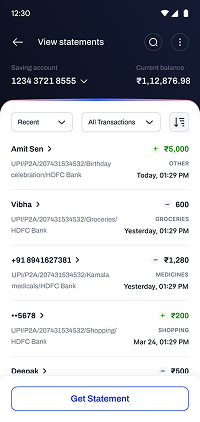

Decision 02

Powerful yet simple bank statement

The existing app had no way to download statements. We introduced downloadable statements with powerful filters and search — by user-created categories, by sent or received direction, and by transaction method (UPI, NEFT, RTGS) — letting users find what they needed without support.

Business Intent

- Statement Download Rate

- Search and Filter Usage Rate

- Support Queries (Statement-related)

-

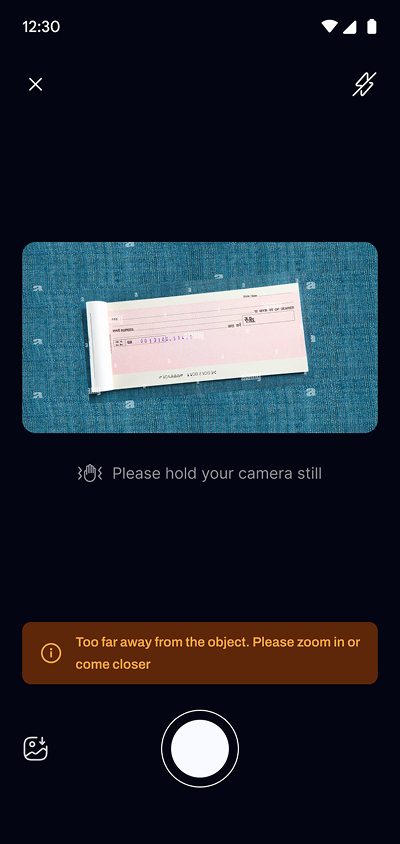

Decision 03

Reducing friction in beneficiary and payment entry

Manual entry of cheque or beneficiary details is error-prone and time-consuming — especially for high-value transfers. We introduced faster, more reliable input methods to reduce errors and build confidence at the point of commitment.

Business Intent

- Transaction Completion Rate

- Input Error Rate

- Time to Complete Transfer

Design System

Building a scalable foundation for consistency and speed

We built an atomic design system from the ground up — covering tokens, components, and interaction states — to ensure every screen felt cohesive and could be built faster across the team.

-

Atom / Colours — Light

-

Atom / Colours — Dark

-

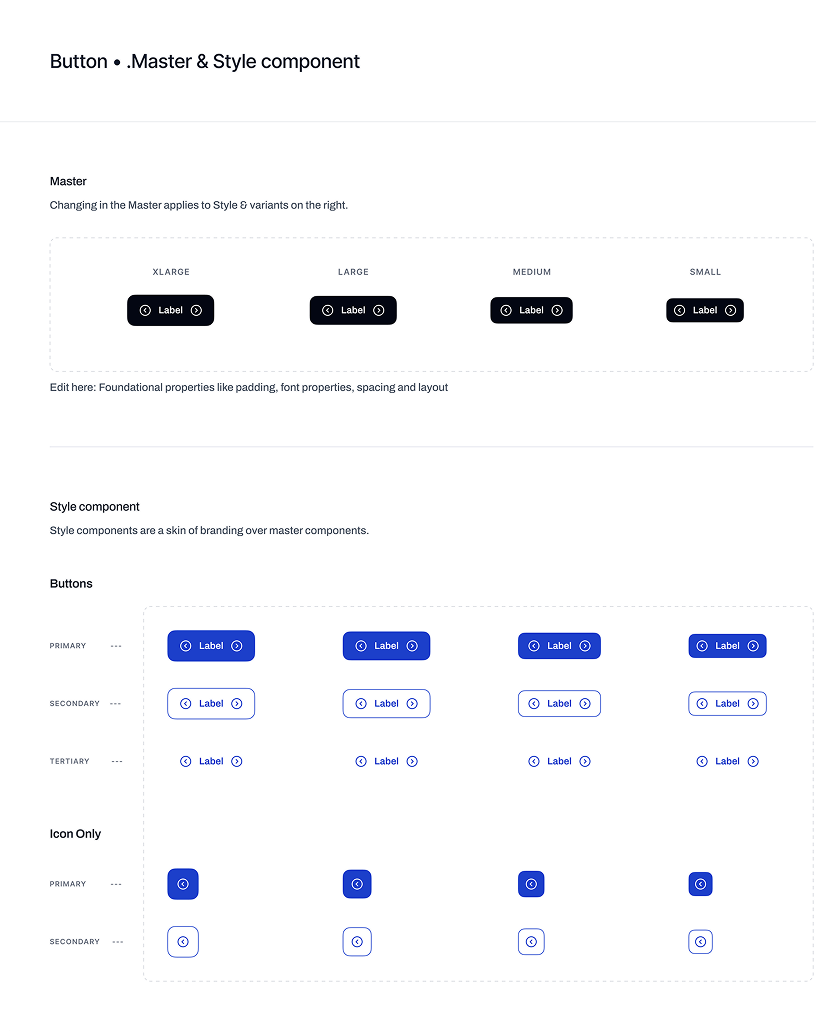

Molecule / Button — Master Component

-

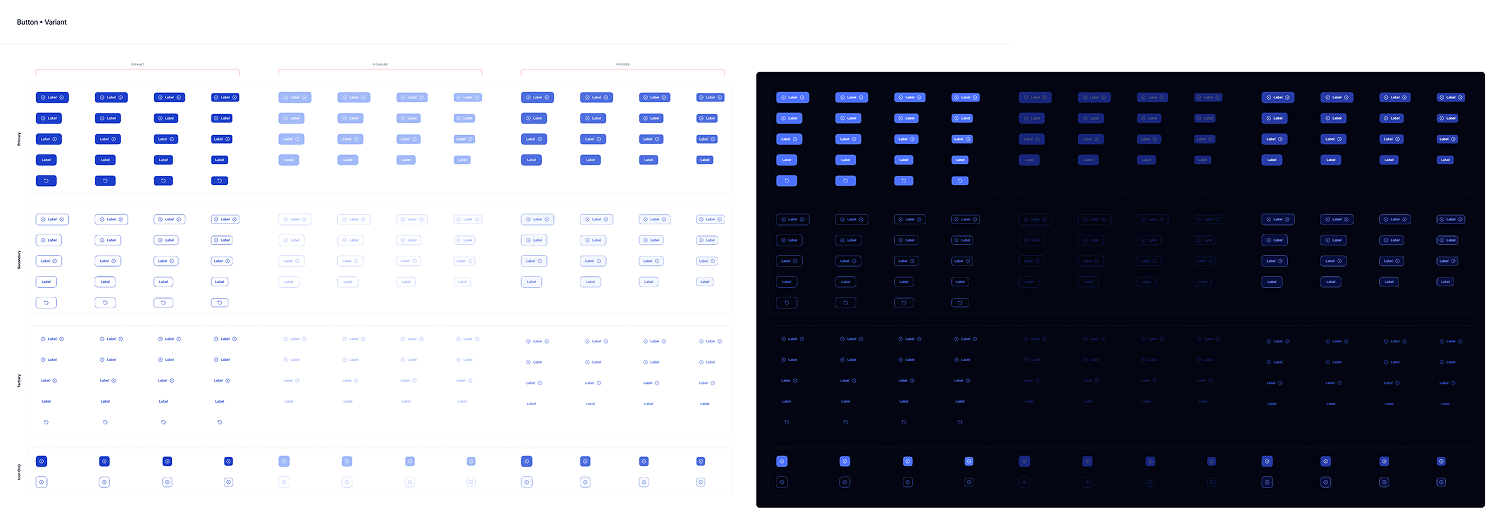

Molecule / Button — Variants

-

Molecule / Button — Redlines

-

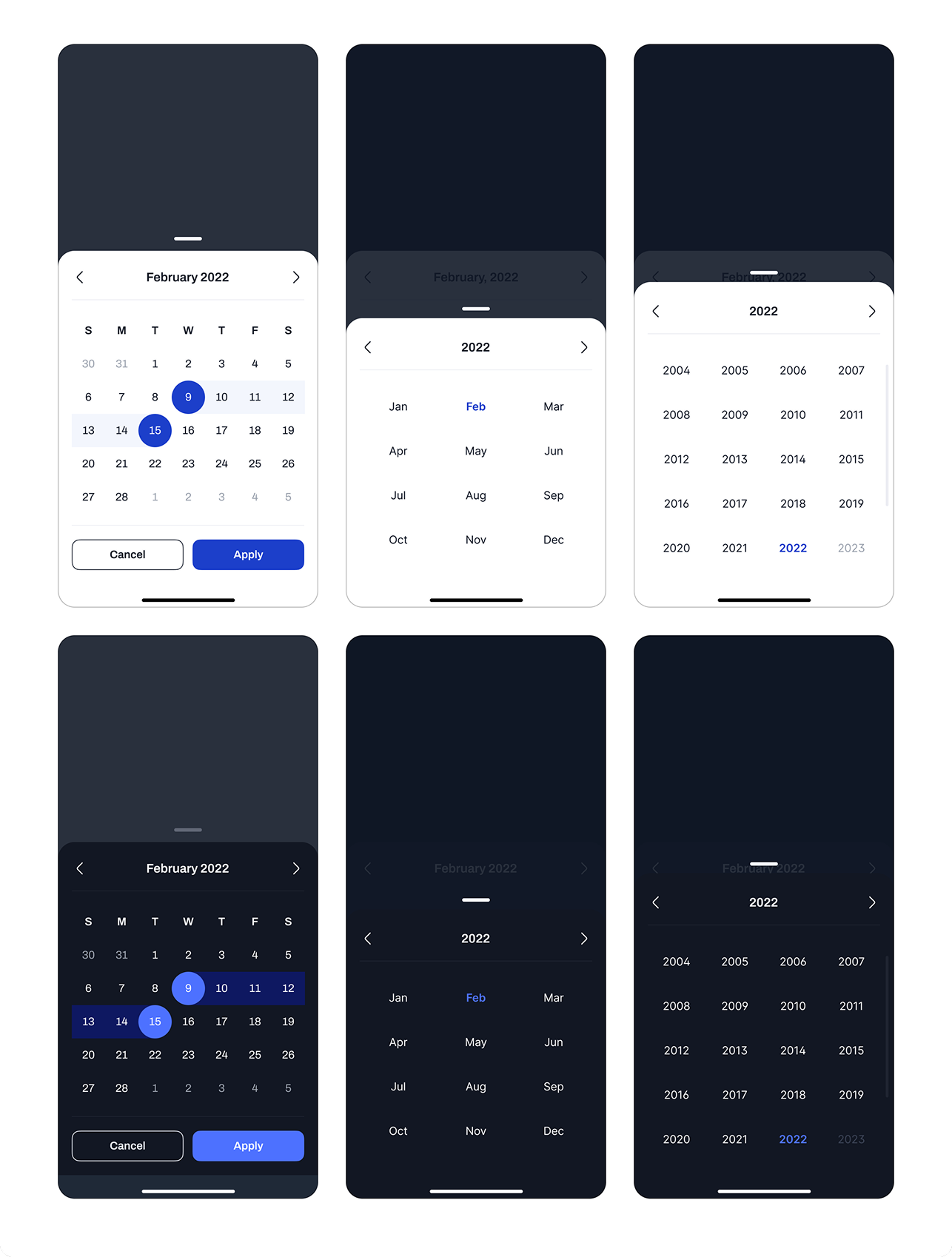

Organism / Date Picker

-

List of Components

The system reduced design time by 50% and is now in use across multiple HDFC Bank products beyond the mobile app.

Testing & Validation

Validating usability across real-world scenarios

Findings & Design Implications

-

Onboarding terminology confused users

System-driven labels in early registration steps caused hesitation and errors.

Language rewritten in plain terms before launch

-

Users gravitated toward lower-friction auth

Strong preference for OTP over more secure but slower verification methods.

Validated the case for pre-login transactions

-

Money transfer entry points were unclear

Users could complete transfers but struggled to find the starting point.

Entry point surfaced more prominently in the dashboard hierarchy

-

Decision-heavy flows caused hesitation

Too many options with unclear labels slowed low-confidence users significantly.

Option count reduced; labels rewritten before launch

-

Statement flows performed strongly

High task success — the design aligned well with user expectations.

Design retained with no major changes

Impact

Driving activation, transaction success, and feature adoption across core journeys

The redesign focused on improving usability across onboarding, transactions, and account management—directly influencing activation, task completion, and adoption of key financial actions. By addressing gaps in clarity, trust, and discoverability, the experience was made more intuitive, scalable, and aligned with user behaviour.

Quantitative Outcomes

-

100%

Successful navigation of the onboarding flow after simplifying key steps — demonstrating low friction in a previously high-drop-off activation journey.

-

~97%

Completion rate on money transfer tasks, validating the unified payment component and improved discoverability of core transaction flows.

-

~82%

Statement task success without assistance — significant given the previous app had no statement feature at all. Users were previously calling support for this.

Qualitative Outcomes

-

Users completed key journeys independently

Real reduction in support dependency — users who previously needed assistance were completing banking tasks on their own.

-

Improved discoverability of critical features

Clearer entry points and better information hierarchy increased visibility of transactions, statements, and filters.

-

Reduced cognitive load across journeys

Eliminating redundant steps and unclear labels improved user confidence and reduced hesitation in onboarding, payments, and account management.

-

Deeper product insights beyond UI

Testing surfaced insights around trust, security perception, and transaction behaviour that shaped broader product thinking beyond the redesign itself.

Social Proof

External validation from users, industry peers, and market adoption

The redesigned experience was not only validated through usability testing but also received strong positive signals from users and industry professionals. Feedback highlighted improvements in clarity, usability, and overall product direction—reinforcing the impact of the design decisions at scale.

Final Designs

Validated design solutions ready for scale

Dashboard Prototype

Registration Prototype